of Manos Hachladakis

"Battle positions" seem to take investors to the Athens market, as the absence of developments (at least positive) in US-Iran relations seems to remove the possibility of finding the gold incision for the end of the war and the placements on the dashboards internationally suggest widespread caution.

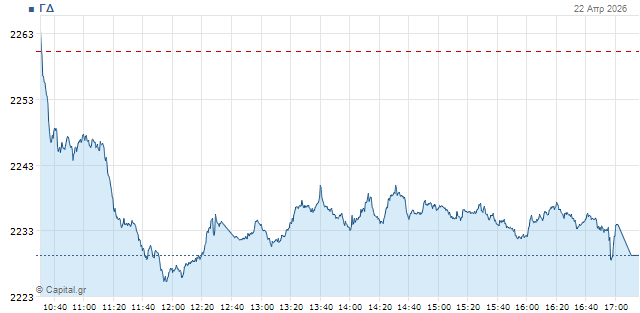

In particular, with the exception of the first two minutes of trade, the General Index was permanently moved to negative territory and completed in 2.229.59 mon. with fall 1,37% (low day at 2.225 Mon.).

Banking index closed on 2,588.95 units with -1,6%, the FTSE of high capitalization retreated to 5,664,8 mon. with -1,46%, while the middle FTSEM recorded smaller losses 0,51% THE 2.843.6 m.

After the fall yesterday at EUR 182.5 million, the turnover was increased but also at low levels of the EUR 232,14 million, of which 20,2 million in 19 packages (1 in PPC for 4,15 million, 4 in Piraeus for 6,9 million, 3 in the EIB for 4.2 million, 3 in Eurobank for 1.7 million) with the volume of transactions in 37,7 million pieces.

The meeting was also marked today by the absence of any substantial interest and the almost total lack of purchasing. The DG quickly retreated, in the first half of the year, to the 2,230 unit area and has since moved "horizontally" at these levels, with placements in higher valuations in the large layers being exceptions.

More generally, if the last hour of Friday's transactions is excluded, characterized by enthusiasm due to the news that the Straits of Ormuz are fully opened (anticipatement cancelled a few hours later only), from last Tuesday's high (14.04) is clear a tendency to restrict positions from some portfolios, while the rest are holding a waiting stop. Something that will hardly change if there are no developments in the US – Iran war issue.

In this regard, the expansion of the truce announced yesterday by President Trump probably increased uncertainty as he avoided giving any timetable, with Tehran appreciating that a surprise attack by American forces is imminent, while arguing that he seized two cargo ships in Hormuz today.

According to reports by Axios, Trump allegedly give Iran 3 to 5 days to return to talksAnd if he doesn't, he'll end the truce. A possibility that if confirmed will mean close meetings by the end of the week (both in Athens and internationally).

Moves on the dashboard

Correctionally, DTP moved together, with losses that exceeded Europeans (Stoxx Banks -0.8%).

Alpha with the biggest turnover of the day at 40.1 million received the biggest pressure with -3.04% retreated to 3.69 euros with -2.4%,

Eurobank (18.9 million) dropped 1.95% to 3.92, the EIB (31.7 million) recorded losses at 1.24% by closing at 14.3 and Piraeus (36.6) retreated to 8.27 to -1%.

Optima (1.6 million) completed at -1.41% and Cyprus (2.3 million) at -0.86%, while only outside DTP Credia with strong profits of 1.97% at 1.24 euros in mixed-value transactions of 5 million

Strong pressure was placed on the title Aegean (4 million) that dived 6.51% at 12.20 euros after the head of Eutytis Vasilakis warned for a difficult one in 2026, with fuel costs and Middle East pressures.

AIA (2.6 million) also closed with -6.02% at 10.30 euros but mainly due to the cut-off of the dividend today €0.662 per share.

Allwyn (7.9 million) was also found in the main options of the sellers with -3,16% at 13,17.

A new strong fall of 2.21% also noted Coca Cola (2.1 million) closing at 48.75 euros, with ELHA (562 thousand) also at -2.33%.

In the few exceptions to the 25-year period provided some support to the DG GEK TERNA (12.2 million) moved to new historically high closing at 41.2 euros and AKTOR (1 million) was strengthened by 1.45% at 11.16.

Just two more titles of the index were positive, Cenergy (2.6 million) with +0.57% and Saranti (391 thousand) with +0.27%.

OTE (6.6 million) marginally lost the mark at the end and EYDAP (420 thousand) had minimal losses (both at -0.11%).

In mid caps, Profile (851 km) was strengthened by 1.33% and IPTO (823 km) experienced a new rise of 0.97%.

On the other hand, sellers focused on Qualco (463 km) at -3.57% and Furlis (222 km) at - 3.25%.

Intralot (2.1 million) made small profits 0.37% at 1.078 euros but completed 7 upcoming meetings.

In the lower layers he distinguished +5.4% of Frigoglass (59 mm), +3.2% of ECTER (536 mm), +2.3% of Real Consulting (173 mm) and +2.2% of Alpha Trust Andromeda (85 mm).

A total of 48 titles were completed with an increase of 79 with a drop (73 unchanged).

International image

After a mild drop by this morning, buyers have taken expected clear lead in oil and prices are now coming back higher than all $100 a barrel.

Brent at $100.4 a barrel with +2% and American WTI at $91.6 with +1.8%.

Similarly, European gas negotiates at 42,4 euros a megawatt hour with a rise of 1.2%.

In shares, Wall Street indicators move upwards after the truce, receiving a boost from some strong corporate profits (primarily Boeing).

Dow Jones at +0.9%, S&P 500 at +0.75% and Nasdaq at +0.85%, in the first half-hour.

In Europe, there is basically a negative sign now, after a limited growth initially. German DAX at -0.3%, French CAC 40 at -0.5% British FTSE 100 at -0.1%, Italian FTSE MIB at +0.1%, Spanish IBEX 35 at -0.5% and the pan-European high capitalization of Stoxx 50 at -0.2%.

In the bond market, changes are marginal. The yield of the ten-year US at 4.27%, the German title at 2.99% and the French at 3.63%, with the Greek at 3.71%.

Finally, rising is the trend in metals after the losses yesterday. Gold at $4,771 an ounce with +1,1% and silver at $78.2 with +2,2%.