LAST INFORMATION 13:10

of Manos Hachladakis

To change course is the Athens Avenue after an initial lead by the sellers, with a background to the change of trend that is being deleted at the last hour in oil prices.

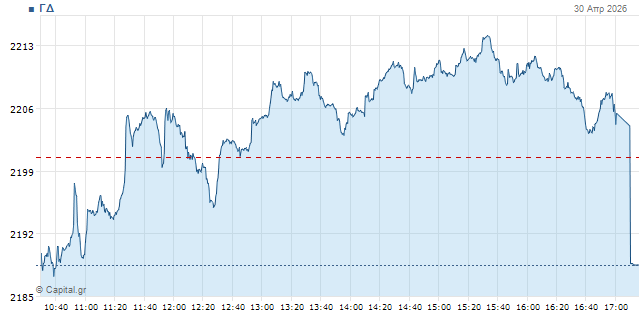

In particular, the General Index moves at 2,208 points with 0.35% profits and the turnover at 82m euros, while 11.5 million pieces have been moved.

The banking index declines by 0.8% to 2,493 units, the FTSE of high capitalization is rising 0.35% to 5.597 mon. and FTSEM of the middle negotiates at 2,858 mon. with -0.3%.

Last meeting in April today, which despite the side-fall traffic in most of it (-3.66% the DG from 15/04 to today) has been a month of recovery thanks to its strong start (+10.87% to 15/04).

Thus, the DG entered trading today with +6.57% in April as a whole, starring as usual the banking industry, since the DTP writes +9,82% in the same period.

From there, the investment interest seems to be decreasing more and more as the days pass without the slightest development on the front of the Middle East, with a characteristic that the turnover on Athens Avenue stayed yesterday at just 171.95m euros.

It was also indicative of the change of just -0.11% by which the DG closed, which "landed" exactly over 2,200 units, receiving support from the Biocos Group (mainly the 6.7% Cenergy rally) and the two refineries benefiting from the ejecting of oil prices.

Brent now stepped on all $120 a barrel, touching high four years (since June 2022 and the initial stage at the time of the war in Ukraine) without any prospect of de-escalation of pressure since the Straits of Hormuz remain "sealed".

However, as mentioned above, in the last hour there has been a trend change with prices now having a negative effect, although no direct correlation has yet been apparent.

In the latest known developments on the subject, however, D. Trump examines a prolonged blockade of Iranian ports, while according to Axios the commander of US forces will present to the president new plans for possible military action.

From there on, the Fed has maintained its interest rates unchanged at yesterday's sitting but with the most enlarged degree of disagreement between its officials since 1992, as they voted in favour of the 8-4 decision. It was also the last meeting of the planet's strongest central bank with Jay Powell at her wheel, who said she would remain at the Fed Board but keeping low tones.

The baton today passes to the ECB, which is essentially a fact that it will not make any interference with its borrowing costs either, with the attention of being focused on the statements made by Governor Christian Lagarde about the future moods of the Eurobank officials at the time the noose of inflation is re-triggered.

As Eurostat has informed today, the IMF in the euro area has accelerated to 3% annually in April from 2.6%, with eject at 4.6% (from 3.4%) for Greece. At the same time, GDP showed a marginal increase of 0.1% both in the euro area and in the EU in the first quarter of 2026 compared to the previous one.

Another point of attention is the barrage of results announcements made last night by companies in the group of so-called "Magnificent 7", with "winning" primarily Google Alphabet, Youtube, Gmail (rally 7% pre-conference) and after Amazon (+2.7%), while Meta Facebook, Instagram failed (-7%) and Microsoft was rather "slip" (+0.03%), while baton passes today on Apple.

Moves on the dashboard

Supports to the DG are mainly given to the refineries which are the beneficiaries of ejecting oil prices.

Motor Oil at 37.8 euros and Helleniq Energy at 9,90 both with profits above 3%.

Biohalco continues from where it finished yesterday with a new +2.9% at 15.30 euros and GEK TERNA also continues higher at 41.18 to +2.8%.

Push to DG also gives +2.2% of Coca Cola, with Metlen at +1.9%.

PPC was found by 18.09 euros (+ 0.72%) but now retreats to 17.86 with the biggest turnover of the day at 10.5 million, due to 4 packages for a total of 390 mm. pieces (a total value of EUR 7 million) that have changed hands at prices from EUR 17,94 and EUR 17,98 per share.

Aegean is under the greatest pressure in the 25th with -3% in 11.1 and EYDAP is retreating by 2.1%.

The sellers also focus on Eurobank that is retreating at 3.72 euros with -1.9%, with Piraeus also at -1.2%.

Mildly droppings move Alpha and ETE to -0.6% and -0.4% respectively.

For its part, however, Axia-Alpha Finance pointed out today that the story of Greek shares remains strong despite geopolitical risks, giving its top picks and dividend leaders.

In mid caps now stands out +2% of Austriacard with Intracom at +1%, while the UAE is retreating by 2.1%.

In total the tableau 57 titles move upwards, against 73 dropouts

The image internationally

Oil prices are moving increasingly high having reached up to $16.4 a barrel for Brent in the morning, but in the last hour there is a reversal of traffic.

Brent at $16 with minus 1.5% and American WTI at $106.8 with minus 0.1%.

At the same time, European natural gas is traded at EUR 47.9 a megawatt hour without substantial changes.

In stock, the American index contracts remain within a narrow range of variations, after another mild downfall on Wall Street yesterday.

Dow Jones' futures at -0.52, S&P 500 +0.1% and Nasdaq at +0.2%.

In Europe some indicators are gradually trying to go on positive ground. German DAX at +0.3%, French CAC 40 at -0.6%, British FTSE 100 at +1%, Italian FTSE MIB at -0.2%, Spanish IBEX 35 at -0.3% and the pan-European high capitalization of Stoxx 50 at -0.2%.

In the bond market returns move slightly lower after the noticeable rise in recent days. The ten-year US at 4.40%, the German title at 3.09% and the French at 3.75%, with the Greek at 3.87%.

Finally, metal attempts to recover after Fed kept interest rates unchanged. Gold at $4,640 an ounce with +1,7% and silver at $73,5 with +2,6%.