LAST INFORMATION 15:45

of Manos Hachladakis

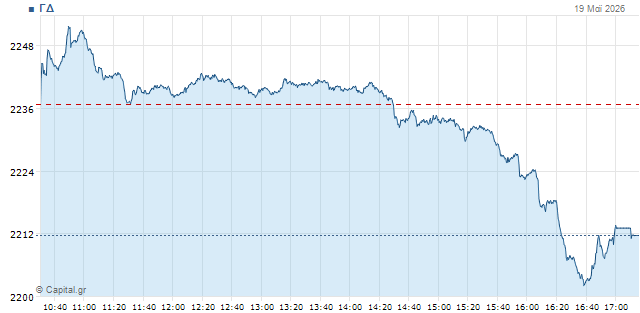

A change of navigation is observed on Athens Avenue with sellers increasing despite the favourable climate on European dashboards.

In particular, the General Index moves at 2,225 units with -0.45% and turnover at 152m euros, while 20 million pieces have been moved.

The banking index yields 0.5% to 2,505 units, the FTSE of high capitalization is falling 0.45% to 5.646 singles, as is the mid-term FTSEM negotiating at 2.944 singles with minus 0.11%.

The attention of the international investment community (and not only) remains focused on the Middle East war, with the latest development of the Trump statement yesterday that it postpones a new American attack planned for today in Iran next – as it argued – a request from the leaders of Qatar, Saudi Arabia and the United States. According to what he wrote on his personal property Truthssocial, these leaders believe that serious negotiations are under way to reach an agreement.

More generally, Trump statements no longer seem to be taken particularly seriously by investors, especially as time passes and are essentially repeated with a periodicity and simply with (about) changed formalities, but even so yesterday seems to give a small "breath" to oil prices and therefore leave a margin to the shares.

Something clearly exploited by European indicators to move higher for the second day, but in Athens the model that appeared in the first half-hour quickly retreated, with banks mainly showing inability to react.

From that point on, attention remains focused on PPC, then on The Commission has therefore decided to initiate the procedure laid down in Article 93(2) of the Treaty in respect of aid granted by the European Investment Bank. Information suggests that offers have already led to three times the coverage (more than 12 billion euros), while it is characteristic that the title price on Athens Avenue yesterday closed at 20.22 euros, at a time when the highest price available to AMC is 19.75.

Another element of interest today in Athens is the move of – the champion of the odds – Biocos Group, who after a while corrected the cluster yesterday (ELHA – 6.4%, Cenergy – 0.96%, Biocos – 1.8%), with only the motherland picking up the recent losses while the other two widen theirs.

At international level, all eyes will turn at night to the US for what has been established in recent years as the investment event every quarter, the publication of Nvidia's financial results.

Moves on the dashboard

All and more are now sellers to banks with only Optima attempting to keep the positive mark on the DTP and the marginal +0.2%.

In systemic Piraeus declines by 0.1%, the EIB by 0.8%, Eurobank by 1% and Alpha by 0.2%.

Outside banks, PPC continues to monopolize the turnover with more than 25m euros, having a mild negative lean at 20.1 euros with -0.6%.

Bioco has an upward reaction of 1% to 18.48 euros, but its two subsidiaries are under new significant pressure. ELHA at 4.9 with a new 6% dip and Cenergy 28.8 at -3.7%.

AKTOR also retreats by 2.8% and GEK TERNA continues to correct for the sixth day at 40.2 euros with -1.8%.

Supports to the DG are Jumbo with +2%, Coca Cola with +1% and Helleniq Energy with 1.3%.

Throughout the board, 43 shares move upwards against 82 pitches.

The image internationally

In the oil market there is a de-escalation of price pressures, particularly for the European slow (and global benchmark).

Brent at $11.2 a barrel with minus 1.7% and American WTI at $107.5 with -1.1%.

European natural gas moves slightly up to 51 euros a megawatt hour with +1.5%.

In the shares, Wall Street indicators lost their initial momentum yesterday with both of the three ending with mild losses (S&P 500–0.07%, Nasdaq–0.51%), while today the contracts are in red for all three.

Dow's futures at -0.1%, S&P 500 at -0.4% and Nasdaq at -0.6%.

In Europe, on the other hand, indicators move for a second day with an upward trend. German DAX at +1.6%, French CAC 40 at +0.8%, British FTSE 100 at +0.7%, Italian FTSE MIB at +0.1%, Spanish IBEX 35 at +0.4% and the pan-European high capitalization of Stoxx 50 at +0.7%.

In the bond market, returns show slight changes. The ten-year US at 4.61%, the German title at 3.16% and the French at 3.95%, with the Greek at 3.84%.

Finally, sellers are also outnumbered today in metals, where gold negotiates at $4,550 an ounce with -0.3% and silver at $76.3 with -1.5%.