LAST INFORMATION 14:00

of Manos Hachladakis

It stabilizes and widens the market lead of buyers in Athens, while the international climate is now more supportive despite the increased risks that have arisen in recent hours for the US-Iran truce.

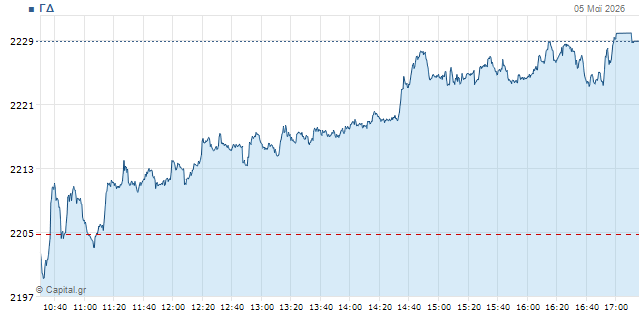

In particular, the General Index moves at 2,217.8 units with +0.6% and the turnover at EUR 90 million of which 16.3 million in 16 packages, while 11.8 million pieces have been moved.

The banking index is reinforced by 1.1% at 2.481 units, the FTSE of high capitalization records a 0.66% rise to 5.619 singles, while the FTSEM of the mid-term negotiates at 2.893 singles with -0.25%.

Athens Avenue shows a willingness to continue for the second day on its upcoming course after yesterday it made a satisfactory reaction (with profits of 0.75% for the DG) after the three-day drop, immediately recovering the level of 2,200 units, in a move that even came against the international downward trend (StOXX 600 -1%, DAX -1,2%, French CAC 40 -1,75%, IBEX 35 -2.4%).

In addition to the first half-hour, characterized by a nervousness and a change of custom, the DG is currently moving permanently positive and could write a much better performance if he was not held back by some show-hard pressures (Coca Cola, PPC, Cenergy).

Substantial difference with yesterday is that buyers seem to be placed more convincing in banks after yesterday DTP marginally won the positive sign (at 2,454.4 units with +0.9%) but interrupted his own five-day downfall streak at the time Stoxx Banks was diving 2.7%.

From there on, the key point of international news is the fact that the truce between the US and Iran seems to be hanging by a thread now, after Tehran attacked the oil plants of Fujira, the United Arab Emirates and the US military sank six small vessels targeting civilian ships, as part of the operation to open the Ormuz. President Trump came back to threats saying that Iranians would be "lost off the face of the earth" if they targeted American warships.

Nevertheless, in the critical for the oil front markets prices have a slightly declining trend, as it seems to have a positive effect on the fact that the shipping giant Maersk announced that an American cargo-vehicle flag of Farell Lines' subsidiary, the Alliance Fairfax, sailed yesterday the Straits of Ormuz escorted US armed forces.

Moves on the dashboard

From where it ended yesterday (+5,7%) Allwyn continues to recover 13 euros with new profits over 2%.

Similarly, Biohalco also makes profits of more than 2% at 15.7 euros, while Cenergy's position in the group's "point" now has ELHA with a 5% rally.

On the other hand, Cenergy shows a mild corrective mood at 24.3 to −0.7% after an impressive six-day cumulative rise of nearly 20% (19.47%).

From then on, banks have a leading role, with EIB and Alpha being strengthened over 1%, while Eurobank moves to +0.9% and Piraeus to +0.8%.

Optima was found to retreat by 8.76 euros (1.76%) but has now turned marginally positive, while Cyprus is strengthened by 1.6%. Better than all moves off the Credia indicator with +2.5%.

Profits over 1% in high capitalization are also noted by Motor Oil and EYDAP, with Metlen at +0.9%.

On the other hand, apart from Cenergy Coca Cola is backing down by 0.6%, despite a strong target price review by Eurobank Equities at EUR 59.5.

PPC remains dominant in the turnover of the meeting, with the packages continuing in view of the 4 billion AMK mammoth. A total of 365 thousand have been transferred to 4 agreed operations. pieces (a total value of 6.6 million) at prices ranging from 18 to 18,13 euros per share.

On the dashboard the title is traded at 18 euros with -1%.

In mid caps that are more subdued activity distinguishes +2.5% of Kri Kri and +2% of Fourli.

Ideal moves at 6,04 euros with +0.6%, while investigating the possibility introduction of ATTIC in Euronext Athens.

Corrective moods show Austriacard with -1.5%, as does Profile also at -1.5%.

In total the table 79 titles are positive, compared to 46 with negative.

The image internationally

As mentioned above oil prices move slightly lower, in the event of gradually restoring traffic in the Straits of Hormuz.

Brent at $131.1 with $1.1% and American WTI at $104.3 with minus 2%.

Small fluctuations in European natural gas, at EUR 44.4 per megawatt hour with +0.5%.

In stock, the American market appears to have a positive model pre-session, after all three indicators with significant losses of 1.1% for Dow Jones yesterday.

Dow's futures today at +0.25%, S&P 500 at +0.35% and Nasdaq at +0.55%.

The European indicators also show a willingness to recover. German DAX at +1%, French CAC 40 at +0.5%, Italian FTSE MIB at +2.2%, Spanish IBEX 35 at +1.5% and the pan-European high capitalisation of Stoxx 50 at +1.3%, while British FTSE 100 is negatively differentiated by -1.1%.

On the bond market, yields slightly decline after the new rise yesterday. The ten-year US at 4.43%, the German title at 3.08% and the French at 3.74%, with the Greek at 3.84%.

Finally, metals attempt to return to positive soil. Gold at $4.555 an ounce with +0.4% and silver at $77.8 with +0.5%.