LAST INFORMATION 16:15

of Manos Hachladakis

Buyers are returning to Athens Avenue en masse shortly before the end of the meeting, after Tehran announced a full opening of the Straits of Hormuz.

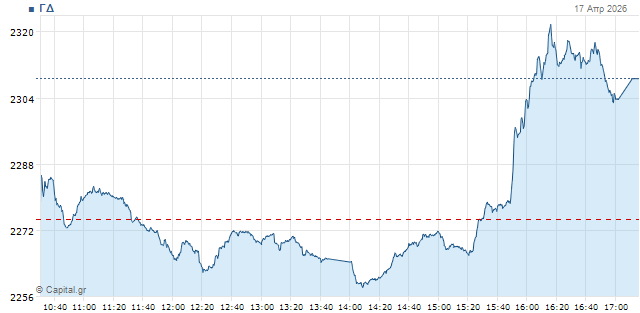

In particular, the General Index now moves to 2,315 points with a profit of 1.8% and turnover at 215m euros, while 32m pieces have been moved.

The banking indicator leads the rise by a 4.3% jump at 2,730 units, the FTSE of high capitalization makes 2% gains at 5,900 singles, while the mid-size FTSEM follows with a milder 0.9% rise at 2,849 singles.

As mentioned above, the landscape not only in Athens but also in markets internationally changed radically after just before 16:00 Iran's Foreign Minister Aragci announced the full opening of the Straits of Hormuz, as long as the Israeli-Lebanon truce is maintained.

Almost directly oil prices were found to take a dive that touches 10%, with the stock indices around the planet taking the wind and Athens Avenue following.

Moves on the dashboard

As mentioned above, the recovery of the domestic market passes through the banking sector, first of all Alpha which makes a 6.8% rally.

Eurobank is reinforced by more than 5%, and the Perais and MIPs above 4%.

In addition to banks, in the 25th leap over 4% is made by Biocos, with Cenergy at +3.6% and Jumbo at +3.4%.

In this climate PPC has erased losses reaching 3.45% (18.48 euros) and now attempts to pass to positive ground.

Expected pressures accept the two refineries, Motor Oil at -3.4% and Helleniq Energy at -2.4%.

Salesmen also insist on OTE with minus 1.9%.

In mid caps it continues to stand out +4% of the UAE at 7.27 euros, with PPA, Furlis and Austriacard all being strengthened above 2%.

A total of 81 titles are moving upwards, compared to 51 fallouts.

The image internationally

As mentioned above, oil prices dive almost 10% after announcements about Hormuz. Brent at $92.5 with -9.5% and the American WTI at $88.5 with -9.7%.

Similarly, European natural gas falls below EUR 40 per megawatt hour, at EUR 39.1 -7.8%.

In the shares, Wall Street indicators moved slightly higher yesterday (wins up to 0.36% Nasdaq) and now their contracts take off shortly before today's trade began.

Dow Jones' futures at +1.1%, S&P 500 at +0.8% and Nasdaq at +0.9%.

Similarly, profits in Europe now exceed 2% on occasion. The German DAX at +2,3%, the French CAC 40 at +2,1%, the British FTSE 100 at +0.6%, the Italian FTSE MIB at 1.9%, the Spanish IBEX 35 at +2,1% and the pan-European high capitalization of Stoxx 50 at +2,1%.

The development with Ormuz sparks massive markets in bonds, with returns now significantly retreating. The ten-year US at 4.23%, the German title at 2.96% and the French at 3.58%, with the Greek at 3.70%.

Finally, powerful upwards are also moving, gold at $4,836 an ounce with +1,2% and silver at $81.5 with +3.5%.

Earlier, at 12:20. the last comment to Capital reported

Despite mild setback yesterday (DG - 0.63%), entering the last session of the Easter week the DG is strengthened by 2.2%, with +3.4% of the DTP driving.

Yesterday, however, the image was diametrically opposite, as banks, following the wider trend of the sector pan-European (Stoxx Banks -1.05%), were pressured (mainly at the closing of the meeting) and escorted the DG to negative ground, combined with the strong fall of PPC (-4.25%) that showed being targeted by a persistent seller after 15:00.

A move that seems to be fully repeated today, after PPC is under new significant pressure and the banks lost their initial dynamics, either partially or completely, going to negative ground.

In any case, with the recovery in Athens being significantly more extensive than the European one, it is more than reasonable to make available profits and portfolio rearrangements, without changing much in the general picture.

In this context, the column pointed out from this morning that it is not excluded during the day that "defensive" moves will prevail, especially in view of any current events that may occur at the weekend.

This is because investors internationally continue to have their attention focused on the Middle East where the Straits of Hormuz remain practically closed, although oil prices move lower. For his part President Trump reiterated once again that the war with Iran is going "extremely" and that "a deal is too close," but investors seem to expect something more clear. It is indicative that the ten-day truce between Israel and Lebanon did not appear to be priced in some way on the stock board, although it is rather a positive development.