of Manos Hachladakis

With a meeting of a prominent nature, the Athens market closed for Easter holidays.

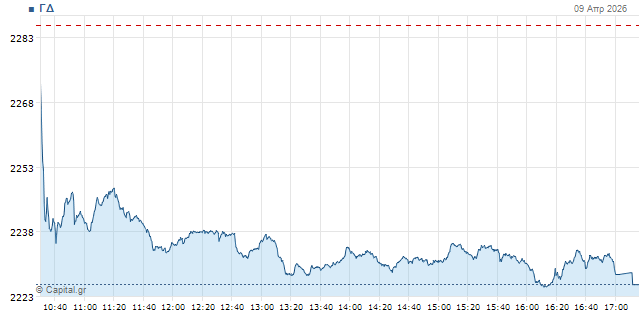

In particular, the General Index was permanently moved with a negative sign and completed transactions on its low day 2. 225,74 units with -2,63%.

The banking index was consistently under the greatest pressure and also completed in its low day 2,531,12 units with -4,51%, as well as the FTSE of high capitalisation in 5,663,91 mon. with -2,83%The midfield FTSEM followed with a more limited fall 1,4% THE 2,707,99 mon. (low at 2.698.09).

After the eject yesterday at EUR 525.96 million, the turnover today rose to EUR 525.96 million. EUR 330,65 million, of which 24.1 million in 20 packages (3 in Piraeus for 3.8 million, 1 in Credia for 7.5 million, 3 in the EIB for 3.98 million, 2 in Optima for 2.3 million) with the volume of transactions in 60.15 million pieces.

In the "cut-off" week of just three meetings due to holidays, the DG came out reinforced against 5,07%, with DTP in +8,19%.

From there on today's meeting of a purely defensive nature, with a clear tendency (degressive) from opening to closing. A rather expected development, based on the combination of great profits yesterday (and a total of 31 March) and the forthcoming holidays tomorrow and Monday, due to the celebrations of Orthodox Easter.

In this context, with great exit opportunities and profit guarantee that reached the previous 5 meetings and 30% in individual titles (Alpha), traders reasonably chose to take defensive positions, especially at the time when the U.S. – Iran truce looks quite fragile.

The same image of caution and profit taking also described transactions on most of the world's board, although with more moderate losses because investors will have the opportunity tomorrow (and Monday) to adjust their positions according to the news that will emerge from the Persian Gulf.

However, the latest developments on the subject show a willingness to respect the ceasefire, with the attacks being significantly reduced today, although Tehran states that Israel is violating the agreed bombing of Lebanon.

Blurry remains the landscape around the critical issue of the Straits of Ormuz, where only a few ships have passed by at the moment, while Russian TASS broadcast that the Iranians agreed to allow transit to just 15 a day.

Moves on the dashboard

The allocation of a profit lock that featured the meeting is evident from the targeting of sellers in best returns titles yesterday and the last five days, primarily of the banking sector (a turnover of 206 million on the DTP).

Alpha with a turnover of 53 million from the top of high capitalization yesterday (+13.06%) was currently found at the bottom with -5,75% at 3.64 euros.

The EIB, with its largest turnover of the day at 55.7 million, retreated to 14.28 euros, Piraeus with 49.4 million at 8.09 with -4% and Eurobank with 39.6 million at 3.73 with -5.09%.

Optima (4 million) also closed to -4.30%, while Cyprus (4.2 million) had the lowest return on the DTP yesterday (+4.5%) today had the least losses with -2.98%.

Outside the index, Credia with the 7th largest turnover of the day at 15.4 million (due to a package worth 7.58 million at 1.12 euros the share) saw orders coming out up to 1.15 (+3.6%) but closed at 1.08 to -2.7%.

In addition to the banks, Allwyn (11.8 million) was also found in the 25th in the target of the sellers with -4.32% at 14.4 euros.

Metlen (18.4 million) retreated to 36.10 euros with -3.17%, but it remains to be seen what impact the publication of its sizes had with EBITDA 753 million in 2025, as it came from a five-day rally 14% (only yesterday +8.9%).

Losses that exceeded 2% in high capitalization still noted Aegean (1.1 million) at -2.26%, Lambda (1.1 million) at -2.19% and EYDAP (554 thousand) at -2.13%.

On the other hand, Hellenic Energy (2.2 million) was positively differentiated to 9.87 with +1.75%, while Motor Oil (17.5 million) deleted profits about 2% in auctions, as they led it to 38.4 to -1.13%.

On the general trend, GEK TERNA (13.1 million) with +1.04% at 38.80 euros, while OTE (7.5 million) at +0.67% and Sarantis (648 thousand) at +0.39% were still on the chart.

In mid caps just a title completed on positive ground, IPTO (764 mm) with +2.03% at 3.02 euros.

Instead, Intralot (1.8 million) corrected to 0.95 with -2.49% and ABax (917 thousand) to 3.04 with -1.1%.

Losses of more than 3% in FTSEM were noted by Greece (140 thousand) at -3.53%, OLTH (79 thousand) at -3.53%, Furlis (100 thousand) at -3.37% and Intracom (307 thousand) at -3.48%.

In the lower layers, traffic against the current followed by Prodea (213 mm) with +6.25%, Interlife (210 mm) with +3.65% and Lavipharm (821 mm) with +2.9%.

A total of 39 titles were completed with an increase of 93 with a drop (69 unchanged).

The image internationally

Oil prices recover to a certain extent after the wild sale yesterday, but are kept in the area of $100 a barrel and lower. Brent at $98.6 with +4% and American WTI at $100.7 with +6.6%.

Similarly, the trend in European gas moving at 46 euros per megawatt hour with + 1.6% is mild upward.

In stock Wall Street moves slightly downhill, after winning over 2.5% for all 3 indicators yesterday.

Dow Jones at -0.15%, S&P 500 at -0.1% and Nasdaq at -0.2%.

The trend in Europe is also declining. German DAX at -1.1%, French CAC 40 at -0.8%, British FTSE 100 around -0.2%, Italian FTSE MIB around the unchanged, Spanish IBEX 35 at -0.4% and the pan-European high capitalization of Stoxx 50 at -0.9%.

The bond market returns are gently strengthened after the sharp deescalation yesterday. The 10-year US at 4.30%, the German at 3% and the French at 3.66%, with the Greek at 3.75%.

Finally, with moderate changes the metals negotiate. Gold at $4.800 an ounce with +0.5% and silver at $75.5 with +0.1%.