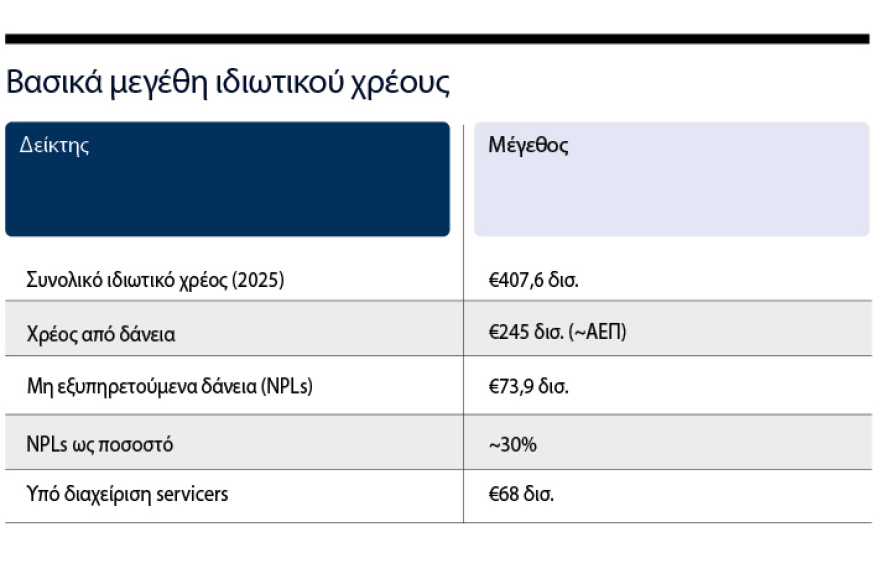

Debt management companies (servicers) cut one in two red loans, trying to address the problem of private debt corresponding to a GDP (EUR 245 billion). Non-performing loans amount to 73.9 billion euros, with 68 billion being managed by servicers. The haircut reaches up to 74% in consumers, 45% in housing and 62% in small business loans. The government is promoting a new digital platform for non-performing loans to operate from autumn, creating transparency in the secondary market worth 80 billion euros.

Analyticalally:

To contribute to a more general trend towards solving the major problem of private debt, the Commission proposes that the servicers, since they account for an important and difficult part of the problem. One in two Loans Now he gets a haircut, they say people who deal with it.

Since the beginning of the debt crisis up to now a large scale of measures, strict and less stringent, has been implemented, and debt recovery is becoming increasingly difficult and require technical and realistic solutions.

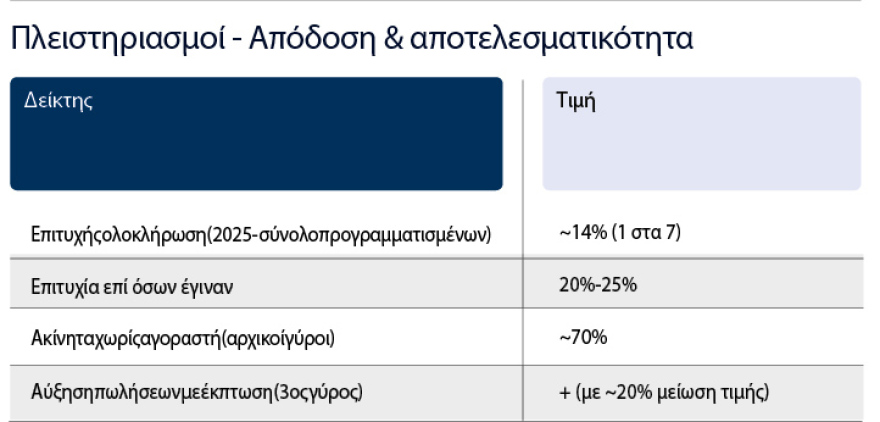

In this direction it moves rapidly and the government is attempting to resolve the thorn of private debt. A total GDP is the total lending in our country, while 1/3 of these loans are red and are in servicers and credit institutions, according to the IOBE bulletin. Based on the same data, only one out of seven auctions are completed.

All of this shows that efforts are needed and a way to safeguard social cohesion, debt management companies to achieve results, but also to ensure that State guarantees for securitised loans are not jeopardised. «Hercules».

The auctions real estate in our country over the last few years have been very fluctuating, reflecting both economic pressures and structural weaknesses in the demand for real estate from this market.

In 2024 it appears to have been a landmark year, as a peak was recorded in the number of auctions, with significantly more properties leading to the sale.

This development is likely mainly linked to speeding up institutional and administrative procedures, but also to pressures on households and businesses from the past, in which debtors did not cope. However, the image differs considerably in 2025.

Although a high number of planned auctions were maintained, their actual completion was limited. Indicatively, just about 1 in 7 properties of scheduled auctions resulted in a successful sale, which translates to close to 14%.

This percentage is set at 20%-25% in respect of the auctions finally held. Total private debt from loans amounted to the third quarter of 2025 to 245 billion euros (approximately one whole GDP), with business loans being the largest proportion.

Non-performing loans account for 30% of all loans held by banks and management companies, reaching 73.9 billion euros, of which the majority (68 billion euros) are managed by the servicers.

Large haircuts and bilateral arrangements are key weapons of debt management companies in recoveries.

More and more borrowers are heading towards the extrajudicial compromise, while servicers are attempting to increase their bilateral arrangements. Reason is one and only: How much it will cost to servicer to recover by auction.

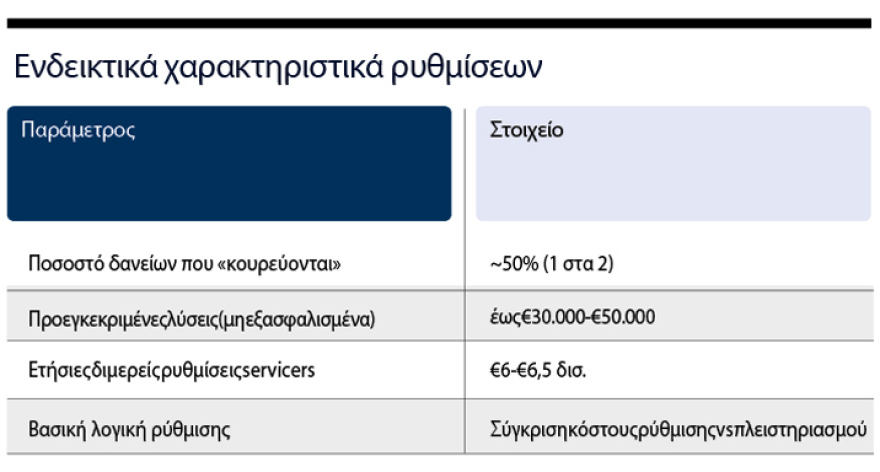

That is the basis of the debate. That is, the failure to make the position of the debt management company worse. Especially in unsecured loans - some companies up to 30,000 euros, others up to 50,000 euros - are offered pre-approved package solutions that provide for significant Haircuts.

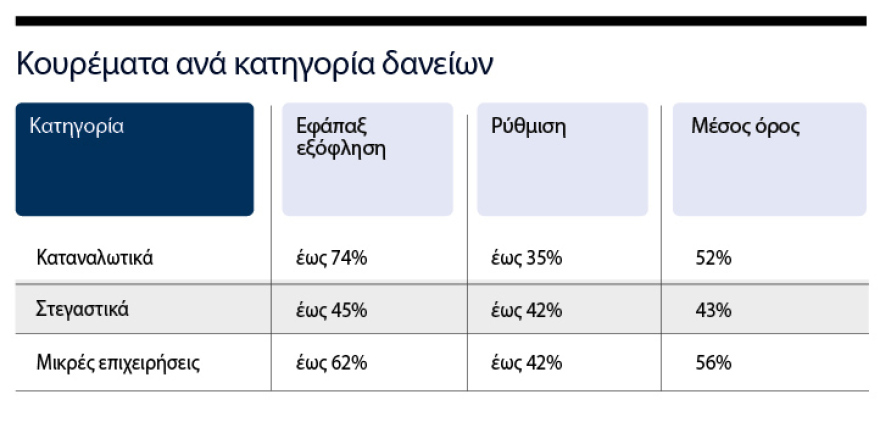

One in two loans, reporting sources with knowledge of the matter, gets cut. In all loans treatment is different in cases where one gives all the amount and those which regulate the total amount.

For consumers in the first cases the haircut is formed up to 74% and in the second up to 35% with an average of 52%. In housing, 45% and 42% with an average of 43% and small business (small business loans), 62% and 42% with an average of 56%.

The bilateral arrangements of management companies are set at EUR 6-6.5 billion per year. The biggest problem that also has a social dimension is certainly housing loans or, more generally, those loans that have property cover.

The morphology of auctions

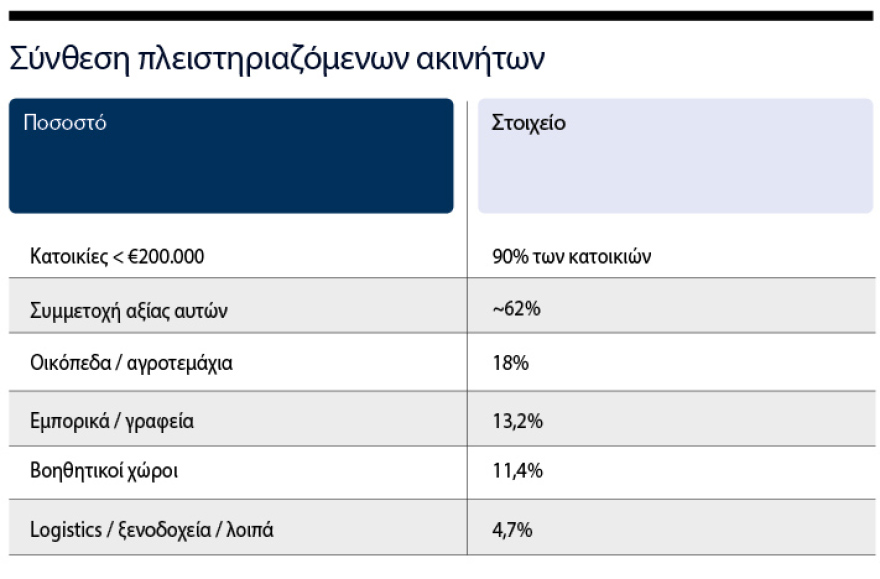

As far as the composition of the buildings is concerned, the large majority concern lower-value housing. In particular, about 90% of the auction houses had a price of less than 200,000 euros, representing about 62% of the total value.

In addition to housing, a significant percentage of the auctions concern other categories of property, such as plots and plots (18%), commercial properties and offices (13.2%), auxiliary spaces (11.4%) and special-purpose properties, such as logistics and hotels (4.7%).

Government initiatives

Throughout the above process and also in the management promoted by the servicers has contributed significantly to the protection net from the government side.

■ The recent regulation, announced by Minister Kyriakos Pierrakakis, allows the debtor to declare that he wants to protect his first residence exclusively even if he chooses to liquidate his remaining assets in order to regulate his debts faster and in more sustainable terms.

■ The programme for converting loans from Swiss franc to euro with a haircut resulting from the rate subsidy is under way.

■ The Interim Programme for State Support is the one which until the operation of the Acquisition and Rerenting Body acts as a tool for supporting vulnerable debtors with monthly aid to the installment of their housing loan.

■ Proceeds the Real Estate Acquisition and Releasing Agency.

■ Significant improvements have been made in respect of the Extrajudicial Debt Settlement Mechanism, with proposals that arise automated and are mandatory by creditors.

■ The Code of Conduct for Banks and Debt Management Companies and Digital Information & Protection from Misuseful Practices has played an important role.

At the same time, the government is also going through another bill where it is preparing, among other things, to make a difference in the amount of debt that can be created by credit cards.

And the other view

The size of the red loans, despite their significant limitation, record an enlarged problem with significant dimensions.

However, one should not overlook that the debt crisis to be solved needed the real help of the State provided with its guarantees. «Hercules».

These remain around EUR 16 billion and concern a number of high-ranking securitisations that could easily be endangered if those who manage red loans do not show the necessary prudence so that this does not happen. A decline in guarantees and the corresponding increase in debt can lead to difficult straits in the national economy achieving a number of upgrades whose benefits are known.

The first public «Marketplace» non-performing loans

Order and greater transparency in «big bargain» Red loans, the total value of which exceeds EUR 80 billion, come to the government, creating the first public platform for non-performing loans since autumn.

A bill put in public consultation by the Ministry of National Economy and Finance makes - for the first time - the state, from a mere regulator, who sets rules on the secondary market for reselling loans, to a manager of the central digital infrastructure in which they negotiate and change hands of loans worth billions.

The purpose of the new platform is to create a public «Information pillar» for loan transactions, but also to facilitate the sale of portfolios between investors (buyers) and banks or services (sellers).

What changes?

Articles 48 and 49 of the new draft law establish that the Non-Served Loan Trading Platform will be established at the General Secretariat for Financial and Private Debt Management. The platform will not be private, but public.

In particular, on this platform:

■ The data of SDR portfolios that come for sale will be published.

■ The negotiation process can be initiated and completed within the same platform.

■ Information on the outcome of SDR transactions will be communicated even if the negotiation process is initiated outside the platform.

■ Information will be posted from other public and private sector bases.

The platform will also record all the earlier transactions completed before it enters into operation, thus creating for the first time a historical record of the Greek secondary market of SDR.

No blind sales.

With the current data, with data from the Bank of Greece for the fourth quarter 2025, loans managed by the debt management companies (servicers) amount to 80.02 billion euros. This is the size of the market for red loans circulating in Greece, changing hands and negotiating on the secondary market, but without becoming visible to the public and without common standards for purposes of comparison, pricing or policy making.

To this day, sellers usually make announcements that they want to sell and there are some private platforms, where through them there is an evaluation of the packages. When the transfer procedure is completed, they shall be entered in the Enemy and Land Register. This information and monitoring is currently done secondary, not directly on a digital platform.

With the new process everything changes: it will start as soon as a seller announces that he wants to sell a package of SDRs. It will be viewed by the interested parties and can be of interest to the market. The negotiation can be made directly on the platform. In the end the result will be recorded, who bought the package and at what price.

As the process becomes public, there will be transparency. All investors will be able to see on a platform what is available for sale in secondary and to do the corresponding moves. Market interest will be able to display funds, banks or other investors (legal persons) of domestic or foreign.

The platform will also allow it to check whether an investor is creditworthy, as it is required to meet specific conditions.

In addition, there will also be data available on the history of transactions, i.e. how much has been sold so far aggregated. It will be possible for anyone to see how the secondary market is progressing as the information is publicly available to the public.

The platform is not working yet, as it is expected from autumn onwards. For its operation, after the law has been passed, a Joint Ministerial Decision will be adopted defining everything: common portfolio assessment standards, how to access investors, sanctions on offenders.

It will also take six months to update and adapt the data of the loans to be sold and an impact study is needed for the use of personal data.

However, a gap observed at this stage is that the platform does not provide that the debtor will be informed when his loan enters the platform, negotiates or changes hands. For tens of thousands of households who often do not even know who their loan belongs to today, this issue remains an open wound.