After a decade «frenzy» Prices rise in purchase of housing In Attica, experts' estimates speak of stabilising values over the next few years in much of the basin.

The real estate market is expected to move at a milder pace in the period 2026-2028, while the course of values will increasingly depend on the quality characteristics of each property and the sizes of each area.

ARTICLE CONTINUES AFTER ADVERSION

The prevailing scenario, as recorded in a study by the Pan-Hellenic Real Estate Network E-Real Estates, includes, among other things, stabilising values in much of Attica, greater negotiation between buyers and sellers and increased importance of energy efficiency, functionality and construction quality.

Areas with increased potential for pressure and price stabilization

The possible corrections are not expected to be horizontal. They concern mainly areas where:

- have recorded particularly high growth rates over the last eight years,

- were strongly supported in short-term lease (Airbnb),

- were significantly affected by investment demand;

- or have a large percentage of old and unupgraded residential stock.

At the same time, they concern specific types of property, such as old houses without renovation, energy-deprecated properties and houses with requested prices that do not meet their characteristics (e.g. Apartments without elevator or parking space).

The image that is being developed refers to a market that becomes more selective, with a greater emphasis on the quality of the property and the value-to-value ratio.

Areas where pressure may occur on housing sales prices during the period 2026-2028

Source: National Network E-Real Estates

Note: Estimates mainly concern old, unrenovated or overpriced properties and do not provide for the total market or transactions in each region. They are based on an assessment of market conditions, taking into account the price and income relationship, real estate returns, supply and demand for housing, as well as the quality characteristics of the available stock.

ARTICLE CONTINUES AFTER ADVERSION

The center of Athens after Airbnb and Golden Visa

The centre of Athens was the «star» of the past decade. The rise in prices was based on short-term lease, Golden Visa, foreign investors, digital nomads and the overall development of tourism.

Today, the market shows signs of ripeness. Absorption times are increasing, negotiation is strengthened and demand becomes more selective. The biggest pressures are expected to concern mainly old low energy efficiency properties rather than quality, renovated housing.

Western Suburbs: when incomes do not follow prices

Aegaleo, Peristeri, Nice, Ilion and Petersburg benefited significantly from the expansion of the metro and the transfer of demand from more expensive areas of Attica. However, in several cases prices increased faster than local incomes. This does not presuppose a general fall, but limits the margins of further strong growth and leads the market to a more stable phase.

Southern Suburbs: strong demand, but not for all properties

The southern suburbs still have strong fundamental characteristics, thanks to the Greek, coastal front, foreign capital, high incomes and limited housing supply. At the same time, however, the market becomes more selective.

ARTICLE CONTINUES AFTER ADVERSION

Old properties in Alimos, Old Faliros or in parts of the Greek that seek prices corresponding to Glyfada or Voula, without corresponding quality characteristics, may face longer disposal times and increased negotiation.

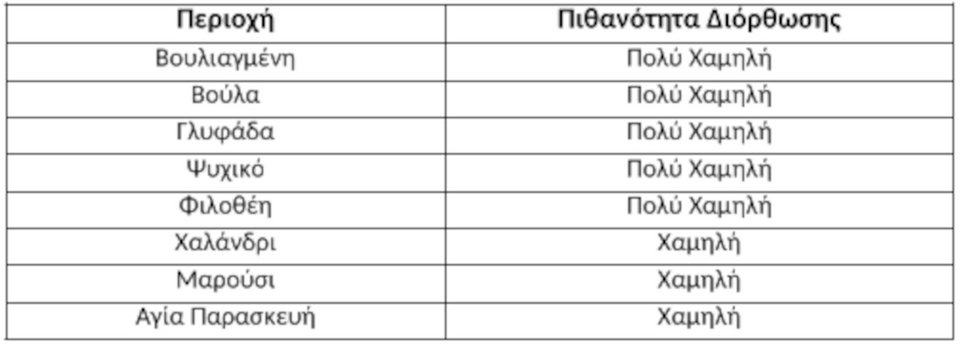

The most durable markets in Attica

«Not all areas are expected to be affected in the same way. The greatest resilience shows markets with high incomes, limited housing supply and timeless strong demand from both domestic and international buyers» explains to iefimerida. gr the president of E- Real Estates, Themistocles Bacas.

Areas such as Vouliagmeni, Voula, Glyfada, Psychic, Philothei, Chalandri and Maroussi have stronger fundamental characteristics, which limits the possibility of significant pressures on housing values even in an environment of greater market maturity.

Areas with the greatest resilience

Source: National Network E-Real Estates

ARTICLE CONTINUES AFTER ADVERSION

The decade of strong rise is coming to an end

The period 2017-2026 is recorded as one of the most dynamic phases of the Greek land market after the economic crisis. Within less than a decade, Attica's housing market went through the recovery phase in a period of severe growth, with sales prices recording significant gains in much of the Lecanope.

In many areas of Athens and Piraeus the requested housing prices increased by 70%, 90% or even more 100% compared to 2017.

Areas such as Koukaki, Pankrati, Metaxorgy, Glyfada, Voula, Greek, Nice, Egaleo and Piraeus were at the heart of this upward course, recording from the highest gains of the last decade.

By area: The main factors that shaped the rise in prices

The upward trend of the housing market in Attica did not have single characteristics in all regions. Each geographical unit followed its own development route, influenced by different economic, social and investment factors.

ARTICLE CONTINUES AFTER ADVERSION

In some areas the rise was linked to international demand and large investments, to others to short-term leases and tourism, while in several cases the new transport infrastructure and demand transfer from more expensive markets played a decisive role.

Southern Suburbs: the impact of the Greek and coastal front

The southern suburbs were one of the most powerful housing markets of the last decade. The great urban regeneration of Greek, the proximity to the sea, the international projection of the Athenian Riviera and the increased presence of foreign investors functioned as the main levers of climb.

Glyfada further strengthened its premium character, attracting both high income buyers and international investors looking for real estate in areas with high quality of life and limited offer.

Voula benefited from the proximity to the sea, the limited available reserve and the timeless preference of higher income households, seeking permanent residence in a quality residential environment.

ARTICLE CONTINUES AFTER ADVERSION

Greek recorded one of the largest price increases in Attica. The expectations created by the country's largest urban regeneration, combined with increased investment interest and the international promotion of the project, influenced the market of the wider region as a whole.

Alimos was strengthened both because of his proximity to the Greek and due to the coastal front, attracting families and investors seeking alternatives to the most expensive markets of Glyfada and Voula.

In the same wider zone, Nea Smyrna, Kallithea and Old Faliro benefited from proximity to the centre of Athens, connection to the southern suburbs and improvement of the infrastructure of the area. Especially Kallithea was positively influenced by the development of the area around the Stavros Niarchos Foundation and the increased investment activity that followed.

Athens Centre: tourism, Airbnb and investment demand

The center of Athens was the major protagonist of 2017-2026. The recovery of tourism, the development of short-term lease, Golden Visa and the increased presence of foreign investors fully remodeled many neighborhoods that until a few years ago were considered undervalued or low investment value.

ARTICLE CONTINUES AFTER ADVERSION

Koukaki was found at the forefront of this change, recording from the highest market value. The proximity to the Acropolis, the development of Airbnb and the intense investment activity functioned as key catalysts.

Το Παγκράτι αναβαθμίστηκε σημαντικά λόγω της εγγύτητάς του στο κέντρο, της αυξανόμενης παρουσίας νέων επαγγελματιών και της γενικότερης αλλαγής της εικόνας της περιοχής.

Το Μετς διατήρησε τον premium χαρακτήρα του, αξιοποιώντας τη μοναδική του θέση μεταξύ ιστορικού κέντρου και Καλλιμάρμαρου, ενώ το Κολωνάκι – Λυκαβηττός παρέμεινε διαχρονικά μία από τις ακριβότερες αγορές κατοικίας της χώρας, με σταθερή ζήτηση από εύπορους Έλληνες και ξένους αγοραστές.

Βόρεια Προάστια: οικογενειακή ζήτηση και επιχειρηματικοί πόλοι

Τα βόρεια προάστια δεν στηρίχθηκαν στον τουρισμό ή στη βραχυχρόνια μίσθωση, αλλά κυρίως στη σταθερή οικογενειακή ζήτηση, στις υποδομές και στην παρουσία επιχειρηματικών δραστηριοτήτων.

Το Χαλάνδρι κατέγραψε σημαντική άνοδο λόγω της πρόσβασης στο μετρό, της εμπορικής ανάπτυξης, της ποιότητας ζωής και της αυξημένης ζήτησης από οικογένειες.

ARTICLE CONTINUES AFTER ADVERSION

Το Μαρούσι, ως σημαντικό επιχειρηματικό κέντρο της Αττικής, επωφελήθηκε από την εταιρική ζήτηση, τις συγκοινωνιακές υποδομές και τη συγκέντρωση μεγάλων επιχειρήσεων στην περιοχή.

Η Αγία Παρασκευή διατήρησε σταθερά ανοδική πορεία, αξιοποιώντας το οικογενειακό της προφίλ, τα σχολεία, το μετρό και τη γενικότερη ποιότητα του οικιστικού περιβάλλοντος.

Πειραιάς και Δυτικός Τομέας: οι μεγάλοι κερδισμένοι των νέων υποδομών

Η λειτουργία των νέων γραμμών του μετρό και η βελτίωση της συνδεσιμότητας λειτούργησαν ως βασικοί μοχλοί ανάπτυξης για πολλές περιοχές του Πειραιά και του Δυτικού Τομέα.

Ο Πειραιάς κατέγραψε από τις μεγαλύτερες αυξήσεις μετά το 2020, επωφελούμενος από το μετρό, το λιμάνι, τις επενδύσεις και το ενδιαφέρον ξένων επενδυτών μέσω της Golden Visa.

Η Νίκαια ενισχύθηκε σημαντικά λόγω της επέκτασης του μετρό και της μεταφοράς ζήτησης από ακριβότερες περιοχές της Αττικής.

Το Αιγάλεω επηρεάστηκε θετικά από τη βελτίωση της προσβασιμότητας, την παρουσία του Πανεπιστημίου Δυτικής Αττικής και την αυξημένη επενδυτική κινητικότητα.

ARTICLE CONTINUES AFTER ADVERSION

Το Περιστέρι, τέλος, αξιοποίησε τη μεγάλη πληθυσμιακή του βάση, το δίκτυο μετρό και τη ζήτηση οικογενειακής κατοικίας, αποτελώντας μία από τις πιο δυναμικές αγορές της δυτικής Αθήνας.

Παρά τις διαφορετικές αφετηρίες και τα διαφορετικά χαρακτηριστικά κάθε περιοχής, το κοινό στοιχείο της τελευταίας δεκαετίας ήταν η σημαντική ενίσχυση της ζήτησης σε συνδυασμό με την περιορισμένη προσφορά διαθέσιμων κατοικιών.

Follow it. on Google News and learn all the news first

See all the last News From Greece and the World,